.png)

The HR Tech SaaS B2B market

# The Strategic Imperative in HR Tech: A Deep-Dive Analysis of the French SaaS B2B Market

**Meta Description:** An in-depth analysis of the French HR Tech SaaS B2B market. Explore market size, go-to-market strategies, competitive dynamics, and AI-driven opportunities revealed by our deep learning models. Your guide to the 2025 landscape.

**Keywords:** HR Tech SaaS B2B, artificial intelligence, AI market analysis, HR Tech SaaS B2B 2025, AI agents HR Tech SaaS B2B, market intelligence, French tech market

\*\*\*

### Introduction: Navigating the Next Wave of HR Transformation

The Human Resources technology landscape is undergoing a seismic shift. Once a domain of administrative back-offices, it has now become a strategic nucleus for competitive advantage. In the dynamic French B2B SaaS market, this transformation is not just a trend; it's a rapidly accelerating reality. Fueled by digitalization mandates, complex regulatory frameworks, and an unprecedented war for talent, the HR Tech sector is burgeoning with opportunity and fraught with complexity.

This article serves as a comprehensive strategic brief, compiling an extensive market analysis into a single, actionable C-suite-level document. Drawing exclusively from a rich dataset processed by our Market Intelligence AI Agent, we will dissect the market fabric layer by layer. We will move from a macro-level panorama of market size and segmentation to the granular tactics of winning go-to-market strategies. We will map the competitive arena, identifying the true holders of power and the disruptive forces challenging the status quo.

Furthermore, we will conduct a rigorous SWOT analysis to uncover the structural strengths and latent vulnerabilities of the sector. Finally, we will step into the future, conceptualizing a suite of specialized AI agents designed to augment human capabilities and unlock exponential value across the HR value chain. This is more than an analysis; it's a strategic blueprint for any leader, investor, or innovator aiming to understand and conquer the French HR Tech SaaS B2B market.

\*\*\*

## Section 1: A Comprehensive Panorama of the HR Tech SaaS B2B Market

The French HR Tech SaaS B2B market is not merely growing; it is undergoing a profound structural evolution. Characterized by dynamism and rapid innovation, this segment is at the epicenter of enterprise digital transformation. The confluence of regulatory pressure, technological advancement, and a post-pandemic re-evaluation of talent management has created a fertile ground for growth, which our analysis indicates is both robust and sustainable.

[PLACEHOLDER - YOUR MARKET URL IMAGE]

### A Market Valued in Billions

Our analysis begins with the market's sheer scale. The **Total Addressable Market (TAM)** for HR Tech SaaS in France is currently estimated at over **€2 billion**. This substantial valuation is propelled by a formidable compound annual growth rate (CAGR) of approximately **15-20%**. This growth is not speculative; it is anchored in fundamental drivers, including the widespread digitalization across small and medium-sized enterprises (SMEs), accelerated cloud adoption, and the increasing strategic importance of human capital management.

The calculation of this TAM is based on a top-down aggregation of industry reports, covering the full spectrum of B2B HR software—from talent management and payroll to recruitment and advanced analytics. From this, we can derive a **Serviceable Addressable Market (SAM)** of **€0.6 billion**. This figure represents the segment realistically accessible to a focused player specializing in AI-powered talent management solutions for French SMEs and mid-market firms with 50 to 4000 employees. The strategic objective, or **Serviceable Obtainable Market (SOM)**, is to capture a significant portion of this, realistically aiming for **€120 million** (or 20% of the SAM) within a 3- to 5-year horizon, a goal achievable through sharp product differentiation and a focused go-to-market execution.

### Decoding the Three Core Market Segments

The market is not a monolith. It comprises three distinct segments, each with unique characteristics, needs, and growth trajectories.

**1. The SME and Mid-Market Engine (60% of TAM)**

This segment, representing approximately **€1.2 billion** of the TAM, is the market's primary growth engine, expanding at **15-20% year-over-year**. These companies (50-4000 employees) are pragmatic and results-oriented. They seek **user-friendly, modular, and scalable SaaS platforms** that can be deployed without significant disruption. A critical decision factor is the ability to integrate seamlessly with their existing payroll and SIRH systems, such as Lucca or Silae.

Their primary pain points are born from inefficiency: **manual HR processes** that create compliance risks, difficulty in tracking employee skills, and struggles with talent retention. They are increasingly drawn to **AI-enabled features** that promise to automate tedious tasks and provide actionable insights. The buying cycle is typically **3-6 months**, involving HR Directors and IT Managers who prioritize ease of use, integration capabilities, and flexible pricing.

**2. The Large Enterprise Bastion (30% of TAM)**

Constituting roughly **€0.6 billion** of the TAM, this segment demonstrates more moderate growth at **10-12% year-over-year**. Large enterprises (4000+ employees) demand **highly customized and comprehensive HR suites** capable of managing a global workforce and navigating complex, multi-jurisdictional compliance. Their needs are less about simple automation and more about risk mitigation, global analytics, and integration with complex ERP systems.

The sales cycle here is considerably longer, stretching from **6 to over 12 months**, and involves a wider array of stakeholders, including Chief HR Officers, Procurement Directors, and IT Directors. Decisions are heavily influenced by vendor stability, market reputation, and the capacity for robust customer support. Objections often center on the high total cost of ownership and the perceived complexity of implementation, making trust and proven performance paramount.

**3. The Niche and Nimble Innovators (10% of TAM)**

Though the smallest segment at **€0.2 billion**, this is the fastest-growing at **20-25% year-over-year**. It consists of specialized vendors focusing on a single HR function, such as recruitment, learning management, or performance analytics. Often serving startups and fast-growing SMEs, these players differentiate through **high specialization, innovation, and superior user experience**.

Their solutions are typically cloud-native, mobile-optimized, and designed for rapid deployment. The buying cycle is short, often **1-3 months**, driven by departmental heads or HR managers seeking to solve a specific, acute problem that their legacy systems cannot address. Decision factors are straightforward: ease of use, cost-effectiveness, and simple integration.

### Key Evolutions Shaping the Future

Our analysis reveals three pivotal shifts transforming the market's DNA:

- **Technological Evolution:** The integration of AI is the most significant disruptive force. Beyond simple automation, **AI-powered HR assistants** are emerging, capable of predictive analytics for talent retention and intelligent workflow augmentation. This is shifting the value proposition from efficiency to strategic intelligence.

- **Regulatory Evolution:** **GDPR compliance** is no longer a feature but a fundamental requirement, influencing product architecture and vendor selection. Furthermore, evolving labor laws in the post-pandemic era necessitate HR software that is not only compliant but also agile enough to adapt to continuous updates.

- **Behavioral Evolution:** The rise of remote and hybrid work models has amplified the need for digital tools that manage a distributed workforce effectively. This includes everything from virtual onboarding to performance tracking and ensuring compliance for remote employees, driving sustained demand for cloud-based HR solutions.

Based on these signals, the market's trajectory points towards a future where **hyper-personalized, AI-driven, and seamlessly integrated modular platforms will define leadership**. Companies that successfully blend deep functional expertise with predictive intelligence, particularly within the underserved mid-market, are best positioned to capture the immense value being created.

\*\*\*

## Section 2: Three Winning Go-To-Market Strategies to Conquer the HR Tech SaaS B2B Market

In a market as segmented as HR Tech, a one-size-fits-all go-to-market (GTM) strategy is a recipe for failure. Capturing market share demands a nuanced, segment-specific approach that speaks directly to the unique profile, pain points, and buying behaviors of each target audience. Our analysis has distilled three distinct, high-potential GTM playbooks.

### Sub-section A: The Agile Growth Playbook for SME & Mid-Market (Segment 1)

This segment represents the largest and one of the most dynamic opportunities. The key to winning here is a strategy that blends precision targeting with value-driven, educational content, all executed with speed and scalability.

[PLACEHOLDER - GTM\_1 IMAGE]

The **ideal customer profile** is a French company, often in Paris or Marseille, with 50-4000 employees and an annual HR tech budget between €100K and €1M. These are typically early adopters of technology, frustrated by the limitations of manual processes and seeking a competitive edge through efficiency. Key buyer personas include the **HR Director**, the **IT Manager**, and the **Finance Controller**, each with their own set of concerns.

The **winning persona** to target is the HR Director. Their three primary obsessions are:

1. **Automating manual tasks** to free up their team for more strategic initiatives.

2. **Improving talent retention** in a competitive market.

3. **Ensuring GDPR compliance** without incurring massive overhead.

The most effective **acquisition channels** are a mix of direct and digital outreach. A direct sales team with a local presence is crucial for building trust. This should be complemented by strategic **partnerships with payroll/SIRH providers** like Lucca and Silae, creating a powerful referral engine. On the digital front, **LinkedIn marketing** and **educational webinars** are paramount for generating high-quality leads.

The acquisition process should follow a clear, four-step cadence:

1. **Awareness:** Use LinkedIn ads and content (whitepapers on compliance, case studies on productivity gains) to attract attention.

2. **Consideration:** Retarget interested prospects with webinar invitations and testimonials from respected HR leaders.

3. **Engagement:** Deploy a 5-touch email and LinkedIn sequence that highlights specific pain points and offers a product demo.

4. **Conversion:** Conduct structured discovery calls focused on solving the prospect's unique challenges, handling objections around data security and ROI, and guiding them to a decision.

The goal is to achieve a **lead-to-meeting conversion rate of 8%** and maintain a **pipeline velocity of 120 days**. With a target Customer Acquisition Cost (CAC) under €10K and an average initial contract value of around €100K, the unit economics are highly attractive. The core insight for this segment is that **trust is built through integration**. Demonstrating seamless, proven interoperability with their existing payroll systems is the most powerful sales tool.

### Sub-section B: The Enterprise Value Playbook for Large Corporations (Segment 2)

Selling to large enterprises is a different ballgame. It requires a relationship-driven, consultative approach focused on risk mitigation, global scale, and long-term value.

[PLACEHOLDER - GTM\_2 IMAGE]

The **ideal customer profile** is a multinational corporation with over 4000 employees, revenues exceeding €500M, and a complex global footprint. These organizations are often risk-averse, with longer decision timelines (6-12+ months) and HR system budgets exceeding €1M.

The primary buyer persona is the **Chief HR Officer (CHRO)**, who reports to the C-suite and is accountable for global HR strategy and compliance. Their obsessions are centered on:

1. **Deploying a scalable, end-to-end solution** that can support a diverse, global workforce.

2. **Mitigating compliance risks** across multiple legal jurisdictions.

3. **Ensuring vendor stability and world-class support** to minimize disruption.

The most effective channels here are high-touch and credibility-focused. **Enterprise direct sales teams** are non-negotiable. This must be supported by a strong presence at major **industry conferences and trade shows**. Furthermore, cultivating a network of **referrals from respected consulting firms** can provide invaluable access and validation.

The acquisition process is a multi-threaded, consultative engagement:

1. **Executive Networking:** Build relationships at the C-level through executive-to-executive outreach on LinkedIn and invitations to exclusive roundtables.

2. **Consultative Discovery:** Engage in deep-dive sessions to understand their complex challenges, particularly around legacy system integration and multi-country compliance.

3. **Custom Demonstration:** Deliver tailored demos that showcase how the platform solves their specific, high-stakes problems.

4. **Stakeholder Alignment:** Systematically navigate the complex buying committee, addressing the concerns of procurement (TCO), IT (security, integration), and HR (functionality, user adoption).

Success metrics shift from velocity to value, targeting the acquisition of 4 enterprise customers over 90 days to generate **€8M in revenue**, with a higher allowable CAC of up to €150K per deal. The key insight is that **enterprises buy risk reduction, not just features**. The winning pitch emphasizes stability, security, compliance, and a proven track record, often validated by analyst reports and major multinational references.

### Sub-section C: The Velocity & Viral Playbook for Niche SaaS (Segment 3)

This segment is about speed, agility, and product-led growth. The GTM strategy must be digitally native and designed for rapid, low-friction adoption.

[PLACEHOLDER - GTM\_3 IMAGE]

The **ideal customer profile** is a tech-savvy startup or fast-growing SME with 10-500 employees. They are agile, move quickly, and have specific, acute HR needs that their current tools can't solve. The decision timeline is short (1-3 months).

The key buyer persona is often the **HR Manager or a Department Head**, who has been empowered to find a quick solution. Their obsessions are:

1. **Finding a turnkey solution** that can be implemented immediately.

2. **Ensuring ease of use** for rapid team adoption.

3. **Achieving their specific goal** without buying a bloated, expensive suite.

Acquisition here is almost entirely digital and community-driven. **YouTube** is a powerful channel for "how-to" videos and software reviews. Active participation in **digital communities** (startup forums, HR tech subreddits) builds credibility. **Google Ads** targeting long-tail keywords related to niche HR problems is highly effective.

The acquisition process is a low-touch, self-service funnel:

1. **Problem-Aware Content:** Create blog posts and short videos that address a very specific pain point (e.g., "How to track engineering team skills for a Series A startup").

2. **Product-Led Exploration:** Drive traffic to a landing page with a compelling demo video and a frictionless free trial or pilot program offer.

3. **Automated Nurturing:** Use a 4-touch email sequence to guide trial users, highlighting key features and integration benefits.

4. **Sales-Assisted Close:** Have a small, highly efficient sales team focus only on high-intent trial users to answer final questions and close the deal.

The goal is high volume: 150 leads and 25 customers in 90 days, generating **€1M in revenue** with a very low target CAC of under €5K. The key insight for this segment is that **the product is the marketing**. An intuitive user experience, seamless onboarding, and a clear, immediate value proposition will drive viral adoption and peer-to-peer recommendations.

In synthesis, while LinkedIn and email are common threads, the messaging and execution must be radically different. SMEs buy **integrated efficiency**, enterprises buy **certified stability**, and niche users buy **immediate problem-solving**. A successful company will master the art of allocating resources and tailoring its approach to capture value across all three fronts.

\*\*\*

## Section 3: Who Truly Holds the Power in the HR Tech SaaS B2B Market?

Understanding the competitive landscape requires moving beyond a simple list of rivals. It demands a sophisticated analysis of the entire value chain, the subtle dynamics of power, and the axes upon which competition truly hinges. In the French HR Tech SaaS market, power is not evenly distributed; it is concentrated in specific stages of the value chain, held by players who have erected formidable barriers to entry.

[PLACEHOLDER - COMPETITION URL IMAGE]

### Sub-section A: The Value Chain and the Locus of Power

The HR Tech SaaS value chain can be distilled into five core stages: **R&D and software development**, **marketing and sales**, **implementation and integration**, **user training**, and finally, **customer support and updates**. While each stage is essential, the true nexus of power and value capture resides overwhelmingly in the first and third stages.

The highest barriers to entry are concentrated in **R&D and software development**. This is where substantial capital investment is required to build a scalable, secure, multi-tenant SaaS platform. More importantly, this is where advanced, proprietary AI expertise—such as the development of an HR assistant integrated with models like Mistral AI—and rigorous **GDPR compliance certifications** create a deep competitive moat. Developing these assets is not only expensive but also time-consuming.

Simultaneously, power is consolidated in the **implementation and integration** stage. Here, economies of scale and network effects become critical. Players like **Lucca** and **Personio** who control **robust integration partnerships** with essential payroll and SIRH ecosystems create powerful lock-in effects. For a customer, the cost and operational disruption of switching from a deeply integrated HR platform are significant. This grants incumbents substantial bargaining power over both customers, who are hesitant to switch, and potential new entrants, who struggle to replicate this ecosystem of partnerships.

Therefore, entities that master both **proprietary AI development** and **deep ecosystem integration** hold the most defensible positions. They control the critical bottlenecks, benefit from high switching costs, and lock in predictable, recurring revenue streams, making this combined stage the undeniable center of gravity for enduring value creation.

### Sub-section B: The True Axes of Differentiation

In this crowded market, competition unfolds along two primary axes that define strategic positioning and competitive advantage. These are not about features for features' sake, but about fundamental capabilities.

The first critical axis is **Product Innovation and AI Integration**. This dimension measures a company's ability to move beyond standard HR functionalities. It's about the degree to which they leverage advanced technologies to deliver modular, scalable, and intelligent platforms. A high score on this axis means offering predictive analytics, AI-driven assistants that automate complex workflows, and a user experience that is not just functional but intuitive. In a market where SMEs demand tangible ROI, AI-powered innovation is the key to creating measurable differentiation and justifying premium pricing.

The second defining axis is **Market Penetration and Customer Traction**. This reflects an organization's proven ability to execute and scale. It encompasses the size and quality of the established client base, the geographic reach, and the strength of the partnership ecosystem. High market penetration provides a wealth of data for product improvement, reinforces brand credibility, and creates a flywheel effect for customer acquisition. It signals to the market that a company has not only a great product but also a viable, scalable business model.

The primary tension in the market exists between these two axes. We see established players with massive market penetration who are now racing to integrate cutting-edge AI, while nimble, AI-native startups possess high innovation but lack the scale and traction of incumbents. The ultimate winners will be those who can achieve excellence on both fronts.

### Sub-section C: Mapping the Key Competitors

Analyzing the competitive set through the lens of these two axes reveals a clear hierarchy of market players.

[PLACEHOLDER - COMPETITION QUADRANT URL IMAGE]

**Leaders (High Innovation & High Penetration):**

- **Personio:** A pan-European powerhouse with revenues surpassing €100 million. Personio exemplifies a leader with its aggressive AI innovation roadmap, end-to-end HR suite, and vast market penetration across the continent.

- **Lucca:** An established French market leader with revenue in the tens of millions. Lucca combines robust product innovation, particularly in time and leave management, with deep market traction and strong payroll partnerships, making it a formidable incumbent.

**Specialists (High Innovation & Medium Penetration):**

- **Zola:** A fast-growing French challenger that has built its strategy around a powerful AI HR assistant. While smaller, with around 15 employees and ambitions of €2 million in ARR, its high innovation potential makes it a significant future threat.

**Accessible Challengers (Medium Innovation & High Penetration):**

- **Silae:** With revenues around €100 million and over 500 employees, Silae is a major force, especially in payroll outsourcing for mid-market firms. Its market penetration is extensive, though its pace of AI innovation is more conservative than the leaders.

- **BambooHR:** A US-based giant with revenues over $100 million, known for its intuitive UX and strong global SME footprint. Its traction is undeniable, but it has a more moderate focus on cutting-edge AI compared to European-native innovators.

- **Payfit:** A well-known player across Europe, strong in HR and payroll automation. It has achieved solid customer growth and SaaS market penetration, but with a more limited set of advanced AI-driven features.

Other notable players fill out the landscape, including **Factorial HR** and **CharlieHR**, who show strong visionary potential but have yet to achieve widespread execution, and established names like **Cegid**, who maintain a steady presence in niche areas but with less disruptive innovation. This mapping reveals a clear narrative: the market is led by those who can pair visionary technology with flawless execution.

### Sub-section D: An Analysis of Market Leaders

The top echelon of the HR Tech market is occupied by a cohort of companies that have successfully blended scale with sophistication. **Lucca** stands out as a prime example of a domestic champion that has achieved leadership through deep market understanding and product excellence. Its strategy hinges on providing a comprehensive, modular suite that solves core French HR problems, particularly around leave and expense management. Lucca's strength lies in its ecosystem; its deeply embedded partnerships with payroll providers create high switching costs and a powerful sales channel, cementing its position in the SME segment.

Alongside Lucca, the broader group of leaders includes global giants and European scale-ups such as **Silae, Workday, Cornerstone OnDemand, SAP SuccessFactors, Oracle HCM, BambooHR, Personio, Talentsoft,** and **Payfit**. While their strategies differ, they share common factors of dominance. Global players like **SAP** and **Oracle** leverage their vast ERP client base to cross-sell comprehensive HCM suites into large enterprises. Specialized leaders like **Workday** and **Cornerstone OnDemand** dominate specific categories like talent management and learning at the enterprise level through deep functional expertise. Meanwhile, **Personio** and **Payfit** have demonstrated how to achieve leadership through aggressive, venture-backed scaling focused squarely on the underserved SME and mid-market segments across Europe. The key to their collective success is a relentless focus on creating integrated, reliable, and scalable platforms that become the central nervous system of their clients' HR operations.

### Sub-section E: A Focus on the Market Challengers

While leaders command the market today, a dynamic group of challengers is actively working to redefine it for tomorrow. The principal challenger, **Personio**, has already ascended to a leadership position but maintains a challenger's mindset with its rapid growth and disruptive ambition. Its success formula combines an all-in-one product offering for SMEs—a segment historically neglected by the giants—with a powerful GTM machine and a clear vision for AI integration. Personio's trajectory serves as a playbook for how to disrupt incumbents by providing superior value to a specific, high-growth market segment.

Beyond Personio, a vibrant ecosystem of promising challengers is emerging. This group includes **Payfit**, which continues to innovate in the payroll and HR space; **Talentsoft**, with its strong focus on talent management; and new-generation platforms like **Workable, Factorial, Hibob,** and **Lattice**. These companies are challenging the status quo in several ways. Some, like **Factorial**, are competing with a highly flexible and modern product architecture. Others, like **Culture Amp** and **15Five**, are carving out highly valuable niches in performance management and employee engagement. Their collective strategy is one of focused disruption. Instead of trying to out-feature the giants, they identify a specific weakness in the leaders' offerings—be it clunky UX, a lack of flexibility, or a high price point—and build a superior solution around it. The primary threat they pose to the established leaders is their agility and their ability to win the hearts and minds of the next generation of HR buyers who prioritize user experience and speed over legacy brand names.

\*\*\*

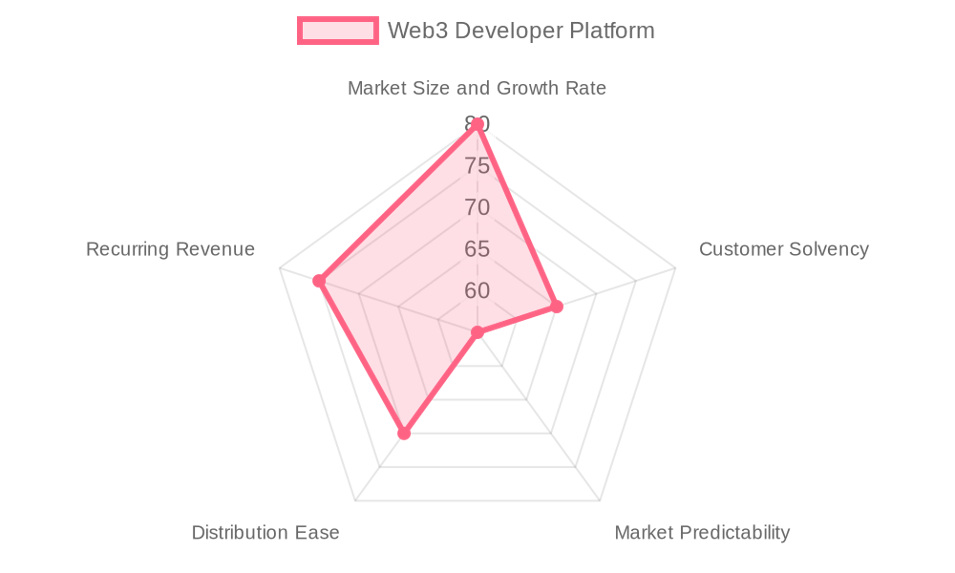

## Section 4: A Strategic SWOT Analysis of the HR Tech SaaS B2B Market

A thorough strategic assessment requires a candid look at the entire market ecosystem—its inherent strengths, critical vulnerabilities, burgeoning opportunities, and looming threats. This analysis synthesizes our data to provide a 360-degree view, revealing the undercurrents that will shape the future of competition and value creation.

### Structural Strengths: The Market's Solid Foundation

The French HR Tech SaaS market is built on a remarkably strong foundation. These are not cyclical advantages but deep-seated structural strengths that ensure its long-term viability and attractiveness.

[PLACEHOLDER - MARKET SWOT URL IMAGE]

First and foremost is the market's **robust fundamental scale and growth**. With a TAM of over **€2 billion** and a **CAGR of 15-20%**, the market provides ample room for expansion. This growth is not a bubble; it is underpinned by the powerful and enduring trend of SME digitalization. Second, the market benefits from **powerful, non-discretionary demand drivers**. The stringent requirements of **GDPR** and the continuous evolution of French labor laws make compliant HR software a necessity, not a luxury. This creates a consistent, predictable demand floor.

Third, the **recurring revenue SaaS model** is a core financial strength. Subscription-based pricing ensures predictable revenue streams, high gross margins (often **80-85%**), and fosters strong customer retention, leading to attractive unit economics and high lifetime value. Fourth, the market exhibits a **high rate of innovation**, particularly with the integration of **AI**. This allows for constant product differentiation, moving the basis of competition from price to value and creating new, defensible moats around proprietary technology.

Fifth, the development of a **strong partner ecosystem** is a significant structural advantage. Integrations with essential payroll and SIRH systems create stickiness and high switching costs, fortifying the positions of incumbent players and creating a barrier to entry for newcomers. Finally, the market is bolstered by a **growing and accessible talent pool**. The combination of HR domain expertise and advanced technical skills, especially in AI and SaaS architecture, available in France provides the human capital necessary to fuel innovation and scale operations effectively.

### Critical Weaknesses: The Market's Hidden Vulnerabilities

Despite its strengths, the market is not without its structural weaknesses. These are vulnerabilities that, if left unaddressed, could constrain growth and expose players to significant risks.

A primary weakness is the market's **intense geographic concentration**. The heavy focus on France, while allowing for deep localization, limits scalability and exposes companies to country-specific economic downturns or regulatory shocks. A second critical issue is the **moderate but meaningful customer switching costs**. While integration creates stickiness, the inherent flexibility of SaaS architecture means that dissatisfied customers can and do migrate to competitors, keeping churn a persistent threat and putting constant pressure on vendors to prove their value.

Third, there is a notable **lack of transparency across the market**. Pricing models are often opaque, and detailed financial performance data for private companies is scarce. This ambiguity makes accurate competitive benchmarking difficult and can cloud investment decisions. Fourth, the **nascent state of advanced AI integration presents execution risk**. While AI is a massive opportunity, the technology is still maturing. Companies that over-promise and under-deliver on their AI capabilities risk damaging their credibility and failing to demonstrate clear ROI, which could trigger customer skepticism.

Fifth, the HR needs of the SME segment are **highly fragmented**. Unlike large enterprises that have more standardized processes, SMEs have diverse and often unique workflows. This forces vendors to build highly modular and configurable—and therefore more complex—product architectures, which can be a challenge to develop and support at scale. Finally, the **intense competition for specialized talent** is a significant constraint. The demand for engineers with expertise in both SaaS architecture and AI, combined with HR domain knowledge, far outstrips supply, leading to high recruitment costs and potential delays in product roadmaps.

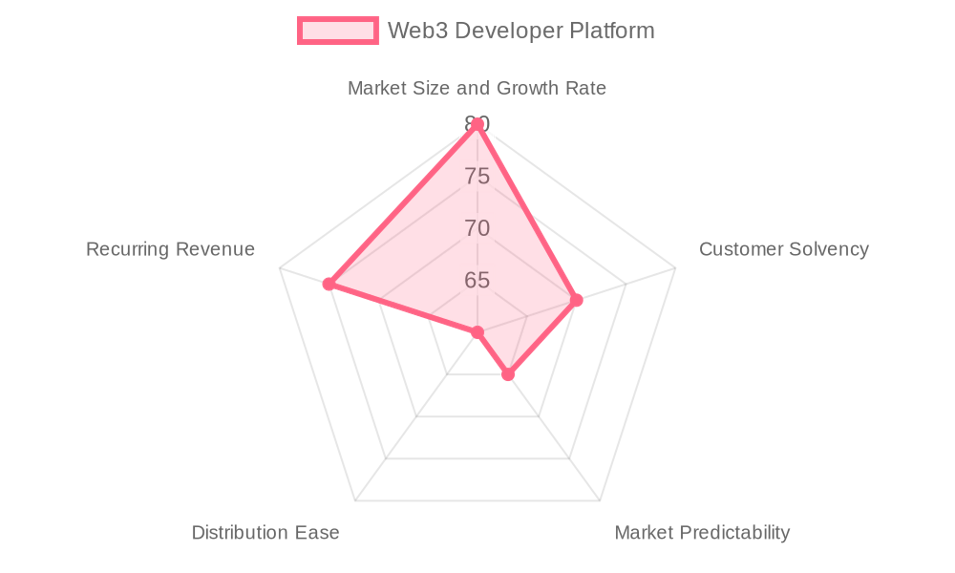

### Sectoral Opportunities: The Catalysts for Future Growth

The weaknesses are balanced by a wealth of opportunities for savvy players who can strategically position themselves to capitalize on emerging trends.

[PLACEHOLDER - MARKET SWOT URL 2 IMAGE]

The most significant opportunity lies in the **continued advancement and application of AI**. Moving beyond basic automation, there is a massive white space in providing **predictive analytics for talent management**. This includes helping SMEs proactively identify employees at risk of churning, flagging skills gaps before they become critical, and optimizing recruitment efforts. This transforms the HR function from a reactive administrative center to a proactive strategic partner. Another major opportunity is **geographic expansion**. For French leaders who have saturated their domestic market, expanding into other European SME markets like Germany, Spain, or the UK represents a logical and potentially lucrative next step.

Third, there is a huge opportunity in **product line extension**. Companies that have successfully captured a client with a core HR module (e.g., leave management) are perfectly positioned to **cross-sell adjacent solutions** such as performance management, learning and development, or employee engagement tools. This not only increases customer lifetime value but also deepens the integration lock-in. Fourth, **strengthening and monetizing the ecosystem** is an untapped opportunity. This could involve creating marketplaces for third-party HR applications or offering premium APIs that allow for deeper, more customized integrations.

Fifth, there's a growing demand for solutions that address **remote and hybrid work challenges**. This creates an opportunity for tools that specialize in virtual onboarding, remote-first performance management, and ensuring compliance for a distributed workforce. Finally, the **potential for market consolidation** presents a strategic opportunity. Larger players or private equity firms can acquire smaller, innovative niche players to quickly gain new technology, talent, or a foothold in a new sub-segment, leading to scale economies and an expanded customer base.

### Global Threats: The External Risk Factors

Finally, market participants must remain vigilant to a set of external threats that could disrupt the current positive trajectory.

The most immediate threat is **intensifying competition leading to commoditization**. As more players enter the market and feature sets begin to overlap, there is a risk of competition shifting from value to price, which would compress margins across the board. A second major threat is **cybersecurity and data privacy breaches**. For an HR Tech company, which handles vast amounts of sensitive employee data, a single significant breach could be catastrophic, leading to massive regulatory fines under GDPR, irreparable reputational damage, and a mass exodus of customers.

Third, the threat of **technological disruption from an unforeseen source** is ever-present. While current players are focused on integrating known AI models, a breakthrough in another area of technology could render existing platforms obsolete. Fourth, **regulatory changes** represent a double-edged sword. While they can be a demand driver, a sudden, complex, and costly new regulation could also impose significant R&D burdens and create compliance risks for vendors.

Fifth, the market is exposed to **macroeconomic downturns**. While some HR functions are non-discretionary, SME budgets are often the first to be squeezed during a recession. This could lead to higher churn rates, slower new customer acquisition, and increased pricing pressure. Finally, a persistent threat is the **scarcity of key resources**, particularly the elite AI and engineering talent required to build next-generation platforms. A prolonged talent war could stifle innovation and make it impossible for all but the best-funded companies to compete effectively.

In summary, the market is a high-stakes arena of opportunity and risk. The recommended offensive strategy is to **double down on defensible, AI-driven differentiation** while building a **robust, integrated ecosystem** to create high switching costs. This dual approach appears to be the most effective way to capitalize on the market's strengths and opportunities while insulating against its inherent weaknesses and external threats.

\*\*\*

## Section 5: Conceptualizing AI Agents for the HR Tech SaaS B2B Market

The true promise of Artificial Intelligence in HR Tech lies not in replacing humans, but in augmenting their capabilities. By handling complex data analysis, automating repetitive tasks, and providing predictive insights, AI agents can empower HR professionals to operate at a more strategic level. Based on our analysis of the market's pain points and opportunities, we have conceptualized a suite of specialized AI agents. These are forward-looking ideas, intended to illustrate the direction in which the market is heading.

[PLACEHOLDER - AGENT LINKEDIN IMAGE]

### Sub-section A: Two Game-Changing AI Agent Concepts

To address the most pressing needs of the SME and mid-market segment, two agent concepts stand out for their potential to deliver immediate and transformative value.

**Agent Concept 1: The "Compliance & Retention Guardian"**

- **Function:** This agent acts as a proactive risk and talent management co-pilot. It continuously scans global and local regulatory databases (for labor laws, GDPR updates, etc.) and cross-references them against the company’s internal policies and employee data. Simultaneously, it analyzes anonymized employee engagement data, communication patterns, and career progression to build a predictive model for churn risk.

- **Job Title Augmented:** HR Director.

- **Problem Solved:** It directly tackles two of the biggest anxieties for HR leaders: the fear of non-compliance and the struggle to retain top talent. It moves these functions from a reactive, manual process to a proactive, automated one.

- **Concrete Use Case:** The agent detects that a new labor law regarding overtime for remote workers has been passed. It automatically flags all employee contracts that need updating, drafts a template for the required addendum, and identifies which managers need to be trained on the new policy. In the same week, it alerts the HR Director that three high-performing engineers in the same team are showing a 75% higher probability of churn in the next quarter, based on reduced engagement and market salary data, prompting a proactive intervention.

- **KPIs Impacted:** Employee Retention Rate, Customer Retention Rate (as compliance is a key feature), a reduction in legal costs associated with non-compliance.

- **Game-Changer Impact:** It transforms the HR function from a cost center focused on administrative firefighting to a strategic asset that directly preserves the company's most valuable resource: its people.

**Agent Concept 2: The "Go-to-Market Opportunity Scout"**

- **Function:** This agent is designed to supercharge the sales and marketing pipeline. It automates the top of the funnel by executing the precise targeting strategies identified in our GTM analysis. It scans LinkedIn Sales Navigator, Google My Business, GitHub, and other alternative data sources for predefined intent signals (e.g., job postings for HR roles, recent funding announcements, announcements of digital transformation initiatives).

- **Job Title Augmented:** Sales Development Representative (SDR) / Marketing Manager.

- **Problem Solved:** It solves the immense manual effort and guesswork involved in prospecting. It ensures that the sales team only spends time on high-quality, pre-vetted leads who have demonstrated a genuine need or interest.

- **Concrete Use Case:** The agent identifies a mid-market company in Marseille that just posted a job for a "GDPR Compliance Officer" and recently upgraded its payroll system. It automatically enriches this company's profile with key contacts (HR Director, IT Manager), flags it as a "Tier 1 Priority Lead," and assigns it to the relevant SDR with a personalized opening line suggestion for their outreach email, referencing the recent changes.

- **KPIs Impacted:** Lead-to-Meeting Conversion Rate, Customer Acquisition Cost (CAC), Pipeline Velocity.

- **Game-Changer Impact:** It industrializes lead generation, creating a predictable and scalable client acquisition engine that allows the company to grow more efficiently and outpace competitors.

### Sub-section B: A Broader System of Conceptual AI Agents

Beyond these two core concepts, an entire ecosystem of specialized agents could be developed to augment every facet of the HR value chain. Here are ten additional ideas:

[PLACEHOLDER - MARKET SWOT PRIORITY URL IMAGE]

1. **Talent Analytics Agent:** Augments the Talent Acquisition Lead by analyzing market data and internal skills to predict future hiring needs and identify critical skills gaps before they impact the business.

2. **Payroll Integration Agent:** Augments the IT Manager by ensuring flawless, real-time data synchronization between the HR platform and various third-party payroll systems, flagging any errors or inconsistencies automatically.

3. **Onboarding Experience Agent:** Augments the HR Manager by creating personalized onboarding journeys for new hires, automatically scheduling meetings, delivering relevant content, and checking in on their progress.

4. **Performance Management Agent:** Augments Department Heads by tracking progress against goals, facilitating continuous feedback, and using performance data to identify high-potential employees for leadership tracks.

5. **R&D Prioritization Agent:** Augments the Product Manager by analyzing all incoming user feedback, support tickets, and market trends to score and prioritize features for the product roadmap, ensuring development efforts align with customer needs.

6. **Customer Support Agent:** Augments the Customer Support Specialist by instantly resolving all Tier 1 queries (e.g., "how do I request time off?") and providing human agents with full context and suggested solutions for more complex Tier 2 issues.

7. **Training & Development Agent:** Augments the L&D Manager by recommending personalized learning paths for each employee based on their role, career aspirations, and identified skills gaps.

8. **Financial Benchmark Agent:** Augments the Finance Controller by comparing the company's key HR financial metrics (like CAC) against real-time market benchmarks, providing insights into financial efficiency.

9. **Employee Engagement Agent:** Augments the Chief People Officer by running automated pulse surveys, analyzing sentiment in anonymous communication channels, and providing a real-time dashboard of organizational health.

10. **Internal Mobility Agent:** Augments the HR Business Partner by identifying internal candidates who are a strong fit for open positions, promoting career growth and reducing recruitment costs.

### Sub-section C: The Future: An Interdependent System of Orchestrated Agents

The ultimate vision is not a collection of siloed agents, but a fully interdependent AI system, coordinated by a central **Orchestrator Agent**. This system would mirror the company's value chain, creating a seamless, intelligent loop of information and action.

[PLACEHOLDER - MARKET AGENT SYSTEM URL IMAGE]

Imagine a system of five specialist agents working in concert:

- A **Customer Success Agent** captures feedback from a client about a missing compliance feature.

- The central **Orchestrator Agent** instantly routes this information.

- The **R&D Agent** receives the feedback, cross-references it with its analysis of market trends, and determines it's a high-priority need. It adds the feature to the next development sprint.

- Once developed, the **Go-to-Market Agent** is alerted and prepares marketing materials to announce the new feature.

- Finally, the **Adoption Agent** creates a micro-training module and proactively pushes it to all relevant users, ensuring they know how to use the new functionality.

This is a vision of an "augmented enterprise," where AI doesn't just perform tasks but facilitates a learning, adapting, and continuously improving organization. The orchestrator ensures that insights from one part of the business are instantly leveraged across all others, creating synergies that are impossible to achieve with human coordination alone. This futuristic model is where the HR Tech SaaS market is heading—a world where competitive advantage is defined by the intelligence and interconnectedness of a company's AI-powered operational backbone.

\*\*\*

### Conclusion: The Strategic Path Forward in an AI-Driven Market

Our deep-dive analysis of the French HR Tech SaaS B2B market paints a clear and compelling picture. We are witnessing a sector in the throes of a powerful expansion, with a **€2 billion valuation and a 15-20% CAGR**, driven by the irreversible tides of digitalization and regulatory complexity. The market is clearly segmented, with the **SME and mid-market** representing the most dynamic battleground, where nimble players focused on AI-augmented, user-friendly, and integrated solutions are poised to win. Go-to-market success is not a matter of a single playbook but of deploying tailored strategies that speak to the distinct needs of each segment—be it the enterprise's demand for stability or the startup's need for speed.

The competitive arena is dominated by leaders like **Lucca** and **Personio**, who have masterfully combined innovation with market penetration. However, their reign is constantly challenged by a vibrant cast of challengers leveraging agility and disruptive technology. A rigorous analysis reveals a market with solid structural strengths, such as recurring revenue models and high innovation, but also critical vulnerabilities, including geographic concentration and the execution risks associated with nascent AI. The path to victory lies in navigating these dynamics astutely.

Ultimately, this analysis confirms a core strategic truth: **Artificial Intelligence is the single most important vector of transformation** in the HR Tech space. It is no longer a futuristic concept but a present-day imperative. The conceptual AI agents we've outlined—from the "Compliance & Retention Guardian" to a fully orchestrated system of interconnected bots—are not science fiction. They represent the tangible next step in a journey toward a more strategic, intelligent, and human-centric HR function.

The market's direction is unambiguous. It is moving towards greater automation, deeper analytics, and predictive capabilities. The most pressing opportunity is to deliver these sophisticated features in a package that is accessible, scalable, and tailored to the underserved mid-market. For the leaders, investors, and innovators in this space, the mandate is clear: embrace an AI-first strategy, focus on creating deeply integrated and defensible ecosystems, and build the tools that will empower the HR leaders of tomorrow. The time to act is now.

\*\*\*

If you are interested in this topic you can follow these next steps:

1️⃣Download below the full HR Tech SaaS B2B market study in pdf format

2️⃣ Get additional insights of this market by reading our memo of an interesting company in this market called Zola (Optimize HR processes with innovative SaaS solutions)

3️⃣ If you want us to build a custom AI system and dedicated AI agents, book a strategic discussion with an AI Partner : https://forms.proplace.co/meet